The mainstream media loves bad news and disasters. As they like to say in the industry, “If it bleeds, it reads.” And if they can scare you effectively, they know you will be back for more. (Horror movies work on the same principle.)

The New York Times recently published an article under the headline “When Moving in Retirement Becomes an Expensive Reality Check.” The couple they chose as the example of a “trend” moved from New York’s Hudson Valley to Colorado 10 years ago; and since then they have relocated from Colorado (their rental price had grown too much) to coastal Florida, where they bought a home, but the neighborhood was filled with “prejudice…and blatant racism”; and then on to New Mexico where they could not adjust to the altitude or climate. They decided to return to the Northeast where, unfortunately, homes in the Hudson Valley had risen beyond what they could afford, and “We had to come down into rural Connecticut, where we didn’t want to be, but here we are because we just didn’t have anywhere to go.” (Editor’s note: I live in Connecticut, and my wife and I often take drives in the country. “Rural” areas of the state are charming and their small towns rival many of those in the Hudson Valley, where I spent a good part of my youth.)

Putting aside the New York Times’ predisposition to identify the most atypical retirees they could find — ones who are discomfited by attitudes and altitudes and may be guided by “champagne taste and a beer pocket” since they can’t seem to afford everything they want — all their issues could have been avoided with a modicum of research. The smartest thing they did in their chaotic journey was to rent their first place in Colorado, which gave them time to decide if the area was right for them. But they apparently did not consider how their budget would cover rental increases; those increases pushed them on to their next stop in Florida, a curious one indeed, about as far away from Colorado in terms of climate, politics and prices as you can get. They were worried about prices and chose coastal Florida, the land of hurricanes, inflated real estate and mind-numbing flood insurance? Yikes.

New Mexico, where I intend to visit in the next year or two — it’s the only state I have never set foot in — was a next choice that demonstrates that the Times’ couple may have had more of a plan to “see the USA/in their Chevrolet” than to settle into a comfortable retirement. But, of course, after dipping their toes in three VERY different locations, they sought to return to where they apparently had been happiest — except, in terms of affordability, the Hudson Valley had moved on from them. The couple had to settle instead for “rural” Connecticut, two hours south, a place they appeared to have a grudge against before giving it a chance.

After they get the sensationalism out of the way, the Times settles in with some advice to other normal retirees. Among the words of wisdom — and common sense — is that, “People often don’t fully research what it would be like to live full-time in their chosen destination.” I am not sure what the Times means by “fully research,” but the most basic research can steer couples away from disaster. Basics include historical climate data (weather.com can help), the politics of a particular town or county (election results are widely available on the Internet), and real estate websites like Zillow and Realtor.com which can keep you updated, literally minute by minute, on how prices are moving in your preferred area. Online magazines like USNews&World Report rank hospitals across the country; Kiplingers is another good source for information specific to retirees.

The featured couple left Florida not only because of their neighbors’ alleged bias but also because of “climbing expenses.” Well, duh, I doubt there have been many retirees in America over the last decade who weren’t aware of the radical increases in property taxes and flood insurance in Florida that blew in with a series of devastating hurricanes. This couple apparently was not aware.

The most helpful, though depressing, story in the article is about the widow who moved from her house in small town Texas and bought a place in Oklahoma to be closer to quality healthcare and entertainment options. But she didn’t sell her Texas home first, and it has lingered on the market, putting her in a financial bind. Her instincts for healthcare access were right; her execution was off. Word to the wise: If you can, sell your primary home before you commit to your next one. And, if you have the wherewithal, rent for at least a few months in your intended area.

The Times’ article implies it is risky business to relocate without doing many hours of research. It’s not. If you know what is important to you, there are plenty of resources available online to guide you to choose the best options. Once you nail down the location that seems right, go visit, ask a lot of questions, be properly skeptical about the answers, and consider renting in the area before you buy.

The Times article indicates that the serial relocators they featured are aiming to fulfill their VA mortgage commitment on the Connecticut house next year and move on, their fifth relocation in a little over a decade. If they hadn’t paid all those moving expenses previously, they probably could have afforded life back in the Hudson Valley, where they were originally settled and, apparently, happy.

My neighbor in Pawleys Island, SC, and I could not be more different. He and his wife live there full time, but my wife and I are vacationers, staying there on average only 10 weeks a year. Gary was born and raised in Columbia, SC, and ran the company his father had started. I was a corporate “weenie” for my entire career, ending it with a short stint at a university and then, in retirement, with a real estate license, this newsletter, a blog about golf real estate and assisting couples to find their dream golf homes. I have no illusions that Gary and I have wildly different opinions and that if we ever discussed politics, it would be a brutal affair.

But we don’t because we both value an enduring friendship that was forged largely in popular music and a little bit of golf. Gary, who is 12 years younger than I, loved the Allman Brothers and other guitar-focused blues and rock bands of the 70s. My music listening roots, though eclectic, were firmly cemented in the mid-60s and college, where I developed a taste for west coast rock —The Doors, the Jefferson Airplane, a less-known group called Love, plus the Beatles and other English invasion bands. (Gary has recently moved to the west coast, musically, with a fascination and passion for The Grateful Dead.)

Over time, I lost a bit of interest in listening to the “oldies” and didn’t keep up with the latest music. Gary, on the other hand, after he left his business, retired to a few hours a day in the wondrous man cave he created in a spare room of his condo. He has the best sound system, headphones and acoustic room I’ve ever been in. And he listens (and watches) every day, via vinyl, YouTube and music streaming services.

We trade stories about music. He is fascinated by this Yankee’s tales of concert going in New York City during the 1960s. He especially loves the story of how I wound up in a tiny bathroom on Bleecker Street in Greenwich Village with Jim Morrison, the famous lead singer of The Doors. To anyone Gary knows, he introduces me as a “guy who once peed next to Jim Morrison.” But a story — actually a recommendation — Gary shared with me about seven years ago awoke my dormant love of music. I had never heard of the blues guitarist Joe Bonamassa until Gary introduced me to his music. He didn’t oversell it before I listened; he didn’t have to. In college, I used to debate with my fellow students who was the best guitarist on the planet, and it typically came down to Clapton, Hendrix, blues guitarist Mike Bloomfield, Alvin Lee of Ten Years After and, occasionally, George Harrison. I dithered personally between a choice of Clapton and Hendrix, but their playing could not hold a guitar pick to Bonamassa’s. And if you like his music, you won’t believe how good it is in a live concert. (I saw him in Hartford, CT, and have plans to see him again at his favorite venue, the Royal Albert Hall in London, next May.)

I will respect Gary’s approach to music recommendations and not gild the lily about Bonamassa. I will let you decide for yourself with this link to a performance of Sloe Gin at the Red Rocks venue in Colorado. (Gary sent it to me.) It starts slow but builds, so hang in there. And enjoy. https://youtu.be/pvvgZMGp5Uo?si=cAx2zvkf822MCM4s

Thanks for reading,

Larry Gavrich

Founder & Editor

Home On The Course, LLC

After 25 years, my wife and I are selling our vacation condo in Pawleys Plantation, Pawleys Island, SC, leaving behind a fabulous golf course, one of the best beaches on the east coast, good friends and lots of inter-generational memories. This month, I recount what we will miss most, and what memories future owners of our condo might begin to build.

Since 2000, my wife Connie and I have owned a three-bedroom, three-bath condominium in the Woodstork Landing neighborhood of Pawleys Plantation in Pawleys Island, SC. Our son was 11 years old and our daughter eight when we purchased the end unit of a six-unit building that had not been built yet. We have used it as a vacation home over the last 25 years. Our two children are now in their 30s and with children of their own – our sixth grandchild was born in early October. The kids live in northern Vermont and Vero Beach, FL, with a child by a previous marriage, my son, living with his wife and two children in New Jersey. As you can imagine, our travel plans have changed significantly over the last decade and the condo is under-utilized as a vacation stop as we travel up and down the eastern seaboard to celebrate births, birthdays and major holidays.

In the coming weeks, we will put our condo up for sale. Although my wife and children agree that it is not smart to spend for something that we cannot use much anymore, the memories make this an emotional decision for all. My son Tim has been obsessed with golf since I stuck a plastic club in his hand when he was four. He had his first birdie at a course in the Myrtle Beach area before he turned 10 and his interest in coastal golf course layouts stoked his interest in golf architecture. When he was 11, he and I won our flight at the huge Myrtle Beach Father & Son Classic. (Truth be told, his age qualified him to play from the front tees and that was a deciding factor in our victory.) Every summer Tim competed against kids his age in the Pawleys Island area’s junior golf program. I am certain there is a straight line between his golf experiences in the Myrtle Beach area and his currently successful career as a golf writer for GolfPass, a division of The Golf Channel.

My daughter Jennie and my wife Connie were smitten with the beach at Pawleys Island since the first time they laid eyes on it. The beach is a mere six-minute drive from the front gate of Pawleys Plantation and, except at the height of the beach season in mid-summer, parking within steps of the beach is easy, and free. (All beaches in South Carolina are open to the public. Even when parking is at a premium, you can find a spot on some beautiful beach along the 25-mile stretch between Pawleys Island and Myrtle Beach.) Jennie did not inherit her fine swimming abilities from me; she earned it swimming in the Atlantic Ocean and in the Pawleys Plantation clubhouse pool, a mere three-minute walk around the pond from our condo.

Pawleys Plantation par 3 13th hole, the “shortest par 5 in Myrtle Beach.

The 18-hole Jack Nicklaus Signature golf course at Pawleys Plantation was opened in 1988. As was typical back then, properties had barely been offered for sale yet; the course was the lure to attract buyers for the adjacent properties. Hurricane Hugo, which severely damaged Charleston, caused flooding and downed trees in Pawleys Island in 1989; I played the golf course a few months after and it had drained well and showed no signs of damage.

In the time since, trees and other flora around the golf course and the community have grown substantially. Today, as you drive through the community’s guarded gate and toward the golf course, you are struck by the effects of the landscaping. Live oaks and other trees form a canopy over many of the side roads; those dramatic live oaks are also a feature of Nicklaus’ layout. In the middle of the par 4 9th fairway, for example, a huge live oak tree, dripping with Spanish moss as well as danger, beckons you to tee it high and hit it high over the top. Doing so will kick the ball down the fairway at least 50 yards farther than if you take the more conservative approach left or right of the tree (or under it, if your worm burner is working well).

Despite warnings in the pro shop and on the scorecard, the Nicklaus layout is not to be trifled with, even though it was softened four years ago mostly with the elimination of a few acres of sand. But the bunkers remain tucked up against most of the greens, and what remains of sand in the fairways can gobble a slightly wayward shot and spell bogey or worse. Because of the tilt of the greens and those adjacent bunkers, the pin positions determine the degree of difficulty for individual holes in ways you won’t encounter at many other courses. At the long par 4 8th hole, for example, a pin on the right side of the green brings bunker in front and lake to the right into play if you are too aggressive. I’d estimate that particular pin position adds an extra half stroke in difficulty compared with a flagstick at front left.

Your enjoyment of a round at Pawleys is dependent on which tees you choose to play, as much as how you are striking the ball. (Some of my more amusing moments in Pawleys Plantation came from sitting on our patio, which has a direct view onto the tee boxes of the par 4 15th hole. The very back tees at Pawleys carry a rating of 74.1 and slope of 144 (before a renovation five years ago, they were even higher). It made me chuckle to see some of the swings on that back tee, knowing full well those optimistic birdie-seeking golfers had their wings clipped during the round.

The 18th hole at Caledonia Golf and Fish Club, view from the clubhouse dining area.

The 18th hole at Caledonia Golf and Fish Club, view from the clubhouse dining area.

Pawleys Island is blessed with some of the best golf on the Grand Strand of Myrtle Beach, which runs about 90 miles from Georgetown, SC to just short of Wilmington, NC. Within a five-minute drive of our front gate, Caledonia Golf and Fish club and True Blue offer two of the most unusual golf experiences anywhere. Both layouts were designed by the late Mike Strantz. Caledonia features lots of sand and water that serve both as challenges and eye candy. You won’t find a golf course with more sand on and around it than True Blue, where half the waste bunkers – golf carts are permitted to drive through them – afford the kinds of lies you’d expect in the fairways. The par 4 18th at Caledonia ends on a 100-foot-long green with the deck of the clubhouse dining area seemingly hanging over the back edge of the green. With an audience, drinks in hand, looking down on you – literally and figuratively – that five-foot putt can look a bit longer.

Pawleys Island may be a resort town – it claims to be the first one on the east coast – but it is situated very well for year-round living. Four of the six couples in our building live there year-round, and my guess is that reflects the overall population of the 900-acre community. Within five miles of our front gate, you have your choice of six supermarkets, including the Whole-Foods-like Fresh Market and a just-opened European chain store Aldi, which features a select discounted line of items. Spring and fall are the high seasons for golf, summer for the beach, and winter for the hardy year-rounders (and a few hardy out-of-town golfers looking for bargain green fees). Our family has spent late December weeks down there, and some years my son and I played golf in shorts and golf shirt and other years in heavy sweaters. On the two or three days a year it snows in Pawleys Island, the snow is gone the next day in all but rare cases.

Restaurants in the area are plentiful, and some of them are quite good. Check out Frank’s, Chive Blossom and Perrone’s for upscale dining; consider the buffet at Hog Heaven for t-shirt and cutoffs dining and some of the best fried chicken east of the Mississippi – all you can eat for $11. Charleston is a little over an hour away and the city maintains, justifiably, one of the best reputations for dining on the east coast.

Healthcare options in the Pawleys Island area are good and getting better every year. Since 2000, we have had to call on the emergency room in Georgetown, eight miles away, for a few minor calamities. The wait times were well within reason and the care as good as we are used to in the ERs of the Hartford, CT, area. Some years ago, while in South Carolina, my left knee gave out. I hobbled around for a couple of days before making an appointment with a local orthopedist. He determined that a cortisone injection would give me relief but that I could very well require replacement in one or both knees within a couple of years. His aim with the needle was true because that was 14 years ago, and I am happy to say that both my knees feel fine today, no replacements necessary. I have returned to that doc for shots in my shoulder and wrist, each time to positive effect. Most specialties in the area are part of the Tidelands Health system which spans Georgetown (Pawleys Island) and Horry (Myrtle Beach) Counties.

If Pawleys Island lacks anything that is important to most of us, it is what to do for entertainment when you are not on a golf course or the beach. There are no movie theaters within 20 miles, and the only live performance theater, in Georgetown, presents sporadic local theater-company shows (and a rare art movie). In terms of visual entertainment, the digital age has been a godsend for those who love Pawleys Island but would miss movies and big-city sporting events. (Note: Through a full-community agreement with cable provider Spectrum, we are billed less than $30 a month for TV, Internet and telephone, although additional payments are made through our HOA dues.). But despite the lack of near-city amenities, the area is blessed with one of the most impressive cultural attractions on the east coast – Brookgreen Gardens, a 9,000-acre sculpture garden with keen emphasis on both “sculptures” and “gardens.” Brookgreen, as well as the big, beautiful beach at Huntington State Park across Highway 17, were donated to the state by Archer and Anna Hyatt Huntington in 1931. Archer was a major philanthropist and Anna a renowned sculptress. There is even a zoo in Brookgreen Gardens where children can get close to the animals. A one-hour boat trip through the marsh is both entertaining and informative about life on the former 19th Century rice plantation.

Have a seat: Just one of the hundreds of sculptures in Brookgreen Gardens.

Have a seat: Just one of the hundreds of sculptures in Brookgreen Gardens.

What I particularly like about Pawleys Island is that virtually everyone you meet is from somewhere else. Our next door neighbors hail from Connecticut – they bought the unit from our former Kentucky neighbors. The others in our six-unit building are from New Jersey, North Carolina (by way of the Caribbean island of Eleuthra), Columbia, SC, and West Virginia. The owners of Landolfi’s, a popular Italian bistro that arguably makes the best pizza AND cannoli in the area, are from outside Philadelphia. A popular grocery store and Italian market is run by folks from New Jersey. And a new meat purveyor in Pawleys Island is called New York Butcher Shoppe, although I have no idea where the owners are from.

A few words about shopping. As with many tourist-dominated areas, Myrtle Beach has its share – some might say more than its share – of outlet shopping malls. I have supplemented my own wardrobe with bargains I’ve stumbled upon while browsing in one of the area’s outlet malls. My latest acquisition was a pair of Travis Matthew golf shoes that retail for around $140. They cost me $80, and they are as comfortable and certainly as fashionable as any I have worn. For those inclined toward standard shopping malls with reliable department stores, Coastal Grand in Myrtle Beach is slightly more than a half hour from Pawleys Plantation, just a mile from Myrtle Beach International Airport.

It will be hard for our family to leave Pawleys Island, but I do not plan on a full separation. I have made a deal with my wife and children that after we sell the condo, I will be pleased to arrange for a week or two in a Pawleys Island house, steps from the beach and a mere 10-minute drive to some of the best golf on the east coast. With grandkids involved now, Pawleys Island could very well become a multi-generational playground for our family for years to come.

Thanks for reading,

Larry Gavrich

Founder & Editor

Home On The Course, LLC

The story has been well told: During the pandemic, the safest refuge was outdoors. But if mountain climbing, spelunking and being out on the water away from crowds did not float your boat, then your most challenging alternative may have been golf. From the pre-pandemic year of 2019 to 2024, golf’s popularity grew by 38%, and total rounds played in the U.S. reached 545 million, a record-setting number. In the first full year of the pandemic, 2020, the number of golf rounds played in the U.S. jumped 13%, according to the National Golf Foundation. Overall, on-course participation nationwide increased by two million, the majority of that coming from beginners.

If you are having trouble in 2025 snagging a tee time the day before you want to play, blame it on the pandemic. If you have noticed a green fee increase every year since 2021, same culprit. If your former four-hour round is consistently longer than four and a half hours, COVID’s to blame for that too. (I recall my first 18-hole round when I shot a 115 and putted everything out, even the one-footers, before I knew better. The adult foursome behind my group of 14-year-olds was livid.)

The beach inside the gates of DeBordieu Colony

The beach inside the gates of DeBordieu ColonyAs green fees have risen at public golf courses, the pandemic’s effect has been even more profound at private country clubs. According to Golf Operator Magazine, initiation fees at many private clubs have tripled in the last five years, with those clubs that formerly charged $5,000 to $20,000 now assessing $50,000 and more. Monthly dues, the operating lifeblood of all private clubs, followed suit, rising from the mid hundreds to well over $1,000 per month. And despite the higher tariffs, private club waiting lists are now the rule rather than the exception.

What is a retired couple to do if their pre-retirement assumptions about private club fees are no longer valid? (That same quandary faces younger families working remotely and planning to move to a community where excellent golf is available inside the gates or conveniently nearby.) The quick answer for all parties on the move is that you have enough exciting options to find the one that works for you, from both social and financial standpoints.

I wrote and published Glorious Back Nine: How to Find Your Dream Golf Home in 2020. What I wrote then about the thought process behind which type of country club to choose is as accurate today as it was back then. Only the price tags have changed. In the book, I identified tangible and intangible reasons for paying more to join a private golf club inside the community where you choose to live rather than opting for daily fee golf just down the road. Here are the tangible reasons:

The chief intangible reason for joining a private club is what I call the “Cheers Bar” effect. Remember the theme song to that overwhelmingly popular show? It ended with, “You wanna go where everybody knows your name.” Of course you do because that means you will be treated with care and respect that cannot be duplicated at most public facilities. Staff at public courses tend to come and go, but the staff at well-run private clubs stick around long enough to get to know your name. Their bosses insist on it.

Your first calculation in deciding whether a private country club is right for you is literally a calculation, a financial one. For those who feel strongly that private club membership is a must, I suggest folding the initiation fee into the total cost of the golf community home you are going to buy. Unless you join an equity club that will return your initiation fee when you leave the club – fewer equity options these days – you can kiss the initiation fee goodbye. But the monthly dues will be a significant part of your budget, and the most important component of your financial calculations to decide whether the private or public option is right for you.

Many of the metropolitan areas in the Southeast, the territory I cover, feature a mix of private and public clubs, and some of the public clubs will feature golf that is as high quality as many of the private clubs. The green fees at the best of the public courses can top out at $100 or more; that provides a good start for comparing the costs of a private club you are considering with the best public golf in the area. Consider the following comparison from my own experience. (I am not a member of either club but I know them well.)

The railroad ties are decidedly Dye at DeBordieu

The railroad ties are decidedly Dye at DeBordieuMyrtle Beach, SC, offers more quality golf per square mile than virtually any other area in the nation. Of its 80-plus golf courses within 60 miles, only a half dozen are private and half of those are located at the far south end of the Grand Strand. Debordieu Colony in Georgetown, SC, features a Pete Dye golf course and a three-mile Atlantic Ocean beach inside its guarded front gate. The layout is one of the best on the Grand Strand, and it shows off most of Dye’s iconic flourishes, such as railroad ties separating green from pond and his signature pothole bunkers wedged into fairways and beside greens. When I last reviewed DeBordieu a little over a decade ago, the initiation fee for a full golf membership was $30,000. Today, the club is charging new members $91,000 and annual dues are $8,640, or $720 per month, which seems super-reasonable given the quality of the club and its robust initiation fee.

Caledonia Golf and Fish Club, in Pawleys Island, SC, is located less than 10 miles north of DeBordieu and shows up on national lists of the best public golf courses in America, most recently at #70 nationwide on Golfweek’s list of “Best Courses You Can Play.” The magazine also ranked Caledonia, and its companion course True Blue, at #4 and #5, respectively, within the golf-rich state of South Carolina. Caledonia and True Blue were designed by the late Mike Strantz whose legendary Tobacco Road and Tot Hill Farm, both in North Carolina, are among the most memorable and talked-about layouts in America. With an annual Caledonia/True Blue membership you will pay $40 each time you play, just $30 in the off season (see annual fees below). It is a great deal for anyone who lives most of the year in the area. If you choose not to purchase a membership, green fee rates range from around $100 in the off season (summer and winter) to $200 in-season (spring and fall).

The following is my back-of-the-napkin calculation of the relative costs of joining DeBordieu compared with Caledonia/True Blue. You can run the same rough exercise with private and public golf clubs in areas you are considering for a golf home. I suggest that my clients consider an initiation (joining) fee part of the cost of the home they buy; a country club membership, after all, hastens integration into the social life of the golf community. And if you are targeting a golf community for your future home, quality golf and an active social life should be high on your list of preferences.

| Club Name | Joining Fee | Monthly Dues | Cost per Play | 16 times per month |

| DeBordieu | $91,000 | $720 | $0 | $720 |

| Caledonia | $2,299* | $192** | $40 | $640 |

*Caledonia’s joining fee – what it calls “membership access” – is a one-time initiation fee.

**The monthly dues amount is calculated by dividing the club’s annual fee of $2,299, for a single member between the ages of 35 and 75, by 12. (Senior member annual rate is $1,699.) Membership applies both to Caledonia and its sister course, True Blue. The major difference between the cost of play at the private DeBordieu and the public Caledonia/True Blue, for those who play four times per week, is in the initiation fee. Other costs are comparable.

The view from behind the 18th at Caledonia Golf & Fish Club

The view from behind the 18th at Caledonia Golf & Fish ClubFor sure there are other private clubs in the Myrtle Beach area that charge lower initiation fees than does DeBordieu, and since all homes for sale in the gated beach community are now listed at $1 million and up, the assumption is that most residents there can afford the fees. There are also other fine public golf courses in the area that do not charge the annual fee that Caledonia does, but their green fees are higher than $40 per play.

In the end, those who don’t have to worry about the relatively steep tariffs at a private club will lean toward the built-in camaraderie, excellent course conditions, a long list of amenities and the upscale treatment by staff and consider the initiation fee no big deal. However, for those with a more modest budget, and who are confident they will be able to build a social network within their new golf community without membership, a top-ranked public course nearby will be a viable option.

Virtually every hole at True Blue golf course is a sandscape

Virtually every hole at True Blue golf course is a sandscapeA recent article at TopRetirements.com ranked the most inexpensive states for cost of living. West Virginia ranked 51st – the District of Columbia was also ranked on the full list – and Mississippi at 50th. I responded to the list with the following published comment:

When I see a ranking list like this, I recall the story of two friends dining in a restaurant, and the one says, "Isn't this food horrible?" And the other responds, "Yeah, but it is the cheapest restaurant in the area." If you have any health issue, or expect you might someday, you'd be nuts to consider any of the states at the top of the cheap-living list. According to the Commonwealth Fund, every one of the top five states is toxic when it comes to healthcare. Commonwealth's 2025 Scorecard on State Health System Performance ranks Mississippi dead last, actually 51st because the District of Columbia is also graded. The most affordable state, West Virginia, is ranked fifth to last. Oklahoma, the fourth most affordable state is also the third most dangerous to your health. Texas, renowned for its zero state income tax, holds down the second worst position for healthcare (and, perhaps, disaster preparedness). Rounding out the top 5 cheapo states, Alabama is ranked 42nd for healthcare and Kansas 33rd. Arkansas, by the way, makes the top five cellar-dweller list for healthcare at position #4. Sharp TR readers might have deduced a common trait among these unhealthy states, besides how much you'd save living there. (Not going to make the obvious political statement here.) But what is truly surprising is that the performance of virtually every Sunbelt state is in the bottom half of the Healthcare Scorecard. I can report that virtually all are located in the Sunbelt, a magnet for retirees because of the weather climate. But the climate for healthcare is a different story.

Lest you think the Commonwealth Fund might be unfair to the states they rank lowest, USNews & World Report ranks Mississippi #50, West Virginia 49th and Oklahoma 48th.

You will find a few excellent hospitals in the Southeast to consider in your relocation plans. They include MUSC Health University Medical Center in Charleston, SC, recognized as the #1 hospital in the state for many years; Atrium Health Carolinas Medical Center in Charlotte, NC, the #1 hospital in the Charlotte region according to some sources; and the Mayo Clinic-Florida in Jacksonville, FL. On a personal note, I once made an unplanned visit to the ER in Georgetown Memorial Hospital in Georgetown, SC and received great treatment. Georgetown is about 50 minutes south of Myrtle Beach.

Thanks for reading,

Larry Gavrich

Founder & Editor

Home On The Course, LLC

One of my favorite websites for “real” information about retirees and their preferences is TopRetirements.com. Recently, the site’s editor John Brady published a group of comments by readers about their searches for homes. I thought some of those comments were worthy of elaboration and response. (I have done some light editing on the questions.)

This is my favorite piece of advice because failure to have “The Talk” before your search commences is the root cause of all failed searches. A move to a community that turns out to be the wrong one for you and/or your partner is an even worse failure than not finding one at all, given the tumult and expense of moving. In the book I wrote a few years ago, Glorious Back Nine: How to Find Your Dream Golf Home, I envisioned the following kitchen table discussion:

Her: “Hon, let’s get serious about selling the house and moving to the Carolinas. We’ve talked about it long enough.

Him: “You’re right. Where do you want to move to?”

Her: “Hmm, good question.”

At the very least, you must nail down the type of area you both agree on – mountains, near ocean and beach, on a lake or some other topography. If you don’t agree on the type of location, your search could be endless and expensive. (It’s a big country out there!) Because of each spouse’s personal preferences or hobbies, you will have some modest disagreements about a final location. In that case your marriage will be tested mightily, in the same way couples describe what it is like to hang wallpaper together. If, for example, he likes golfing and she likes gardening, find a community with a good golf course and a home with a backyard or community plot for gardening – and some local restaurants and entertainment venues you can enjoy together.

You shouldn’t have to travel to find out the distance from your community of interest to a shopping mall; you can do that online with Google Maps or any other map program. But when you do visit a community, insist on a meet-up with local residents; the best communities offer access to “Ambassadors,” typically a couple that will have dinner with you, give you a personal tour of the community and answer all your questions. My experience is that Ambassadors are not shills for the community; they tend to answer even tough questions directly and honestly…as long as the questions aren’t subjective, such as “Are people friendly here?” (Answer: People are friendly everywhere, if you are.) And if you are serious about the community, insist on copies of the HOA documents, such as by-laws and master deed. (See below.)

Amen to that! Many HOAs have the richly deserved reputations typically reserved for state and federal bureaucracies. They are often run by people who think their retirements should be filled with making decisions on behalf of others. Most state laws give HOAs way more power than they deserve. Read the HOA documents closely for the community you are considering and pay particular attention to definitions of things like “common elements,” which are the responsibility of all members of the association to pay to maintain. Our own neighborhood HOA decided that all residents should pay for damages incurred to our neighbors’ “limited common elements” (second-floor porches); that resulted in a $14,000 assessment for each household but a benefit only for those with the problem. Fighting the unfairness of that was a losing battle because the state law gave the HOA the power to impose the assessment on everyone and, surprise, the board members all had damaged porches.

If that were true, most people would stay where they have lived for decades and gotten used to the hot days and bugs. There are plenty of warm climate locations that are free of mosquitoes and other bugs. As for hot and sticky days, air conditioners help.

Excellent advice, doc. Not everyone can rent for a month or two but at least they should spend a long weekend courtesy of a reasonably priced Discovery Package offered by many communities. (Discovery Packages are designed to treat you like a resident/club member and make sure you leave with a good understanding of what you are in for – or a firm resolve to look elsewhere.)

These comments remind me of the couple I worked with years ago whose specific guidelines were “two-bedroom home and a hotel nearby.” When I asked why, they responded that, “We love our children and grandchildren, and we want them to visit often. But we don’t want them staying under our roof. Retirement is for relaxation and not a lot of noise.” In other words, move for yourself, not your kids. You earned it. When our own children were pre-school, we spent many summer weeks on the Carolinas coasts. When it came time to consider a second home, we chose a condo in a golf community that appealed to my son and me for the golf but was just six minutes away from an Atlantic Ocean beach, a strong incentive for my wife and daughter. (Note: We are perfectly content these days to have our kids and their kids stay with us, but when it gets noisy, I do understand the need for some privacy.)

Sorry, but state income taxes can be a fool’s gold. Florida charges no income tax, but its overall cost of living is slightly above the national average because of high property taxes and homeowner and flood insurance rates. Focus on total cost of living, which comprises property and sales taxes, the price of gasoline and other goods and services, and whether senior citizens receive a financial break from the state and local governments. You also can and should put a price on convenience – such as distance to supermarkets and other necessities – and on your health today and in the future (proximity to hospitals and doctors who specialize in whatever ails you -- or might ail you in your retirement years).

Many couples believe that the hard work they have done in their careers and family-raising requires a move to a new location and better climate. But the town/area they have lived in for decades should be a top contender for their retirement years, especially if they have friends, family, trusted doctors and other services in the area; those are as fundamental to their health and happiness moving forward as 70 degrees in January. Vindicate the hard work you have done by at least considering remaining in place and traveling the world. As Bob Dylan once wrote/sang, “Don’t go mistaking paradise for that home across the road.”

Thanks for reading,

Larry Gavrich

Founder & Editor

Home On The Course, LLC

Happy New Year to everyone. To start the year, I am providing about double the content of a typical Home On The Course newsletter. I hope the information is useful to you.

The latest migration reports are in from major U.S. moving companies, and peoples’ reasons for moving to some states are hard to divine.

I looked at reports from Atlas Van Lines, published just before the end of the year, and UHaul and United Van Lines, which were reported in the last couple of weeks. Respectively, the most net migrations by state were to Arkansas, South Carolina and West Virginia. That is a bit of a head scratcher: Those three states rank low in terms of employment, their economies and the quality of their public-school systems – data that cover the reasons why most people relocate. Of course, “closer to family” is another top reason. (Source: USNews & World Report)

At #36 of 50, South Carolina ranks slightly higher than the other two states in “employment” (availability of jobs). It also ranks 33rd in its “economy, which beats out Arkansas (40) and West Virginia (48). Arkansas (38th) is modestly better than South Carolina (42) in terms of its schools, while West Virginia ranks a paltry #48. (Note: A Newsweek “quality of life” ranking placed West Virginia in 49th place, just behind Mississippi.)

The mountainous West Virginia – what John Denver described as “almost heaven” in his famous Country Roads – is, indeed, a beautiful state, but behind its skin-deep beauty are obviously some fundamental issues. Yet those reading this who think the grass is greener in, say, South Carolina and Arkansas may not have done their due diligence in terms of insurance costs and the rising likelihood of natural disasters. Hurricanes that have made landfall in South Carolina and the consequent flooding have helped push insurance rate increases up by double digits in each of the last few years. And although Arkansas may not make national headlines for tornadic activity, it suffered 52 tornadoes last year, an average of one every week, its highest number in more than a decade.

United Van Lines reported significant net migration to the cities of Wilmington, NC, and Myrtle Beach, SC, both at 80%. Yet late last year, North Carolina’s insurance companies asked for a 50% increase in property insurance rates in the Wilmington area; and Myrtle Beach residents are already paying 2 ½ times the national average for property insurance, a total of $4,820. And that does not factor in extra flood insurance required for those homes deemed at risk for flooding by insurers and FEMA. (See article below.) Those realities should make some retirees think twice about where to retire.

Some of the other states ranked in the top 10 for in-bound traffic are equally surprising. The Atlas Van Lines report lists Rhode Island (#2), Maine (7) and Connecticut (8) among the top 10. As recently as three years ago, the news media in Connecticut, where my wife and I maintain our primary home and where we raised our children, were shouting about people leaving the state. But with an economy ranked by USNews at #17 and public schools ranked #8, the headlines have quieted. (Note: I know from personal experience in the Hartford, CT, area that the state’s #3 rating nationally for the quality of its healthcare is more than justified.)

The van line reports are more interesting than they are conclusive. They measure only the locations to which they move customers, a vast minority of the numbers of people moving across the nation. But they do raise questions about what kind of research people undertake before they make consequential moves, and what their motivations might be. They can’t all have relatives in West Virginia.

*

As a related footnote that things may not be exactly as they seem in West Virginia, it might surprise some to learn that John Denver’s Country Roads was written mostly by a lyricist from Massachusetts and that the line “Blue Ridge Mountains, Shenandoah River” describes the area immediately to the east and west of Interstate 81; the Shenandoah Valley and Blue Ridge Mountains are in Virginia, not West Virginia. It is entirely possible that the song refers to “west Virginia,” not West Virginia, a credible notion since Denver and his lyricist never set foot in West Virginia.

Remember the old joke that, someday, because of California earthquakes, people living in Las Vegas would eventually own beachfront property – on the Pacific Ocean? The unspoken corollary, of course, was that those currently living beside the ocean would become homeless, or worse.

Although the beachfront-property-in-Vegas riff is still a far-fetched joke, what is happening on the coasts of the U.S., and in other areas vulnerable to much more than earthquakes, is no laughing matter. As they pay out more and more claims for damages caused by natural disasters, insurers are raising rates significantly and, in a troubling number of cases, dropping their coverage altogether.

If you are unlucky enough to own a home in a high-risk location, you likely have felt the pain already. But if you haven’t received a letter from your insurer yet, imagine that you might lose your insurance on a home because of the risk of hurricanes, flooding, wildfires, tornadoes or other potential disasters. Not only could you be forced to self-insure a home that would cost hundreds of thousands to replace, but anyone who might buy it from you would have trouble finding a mortgage company to lend them money if an insurance policy can’t be written for the house.

For some homeowners who hold mortgages, the story is just as bad. Take, for example, Mike Patterson, a teacher in California whose insurance saga was covered by the San Francisco Chronicle. His longtime federally backed insurance policy was cancelled through no fault of his own.

“…[Patterson’s] longtime insurer, California Casualty of San Mateo, was downgraded by a credit rating agency,” the newspaper reported. “As a result, his federally backed mortgage lender would no longer accept his insurance.”

Patterson had no choice but to sign up for coverage from California’s insurer of last resort, the state-backed FAIR Plan.

“Now he pays just over $1,400 for insurance through the FAIR Plan,” according to the Chronicle. “That’s double what he used to pay to get just a fraction of the coverage, and unlike his old insurance, it covers only issues caused by fire.”

Folks who live in the bucolic areas of western North Carolina could not have imagined that natural disasters would cause them to lose their homes, or that they were not covered in total by their insurance policies. And from a hurricane…400 miles from the point of landfall on the Florida coast? Yet the after-effects of Hurricane Helene, which made landfall in August last year where the panhandle of Florida bends to the west, caused billions of dollars in damage and ruined the fortunes of many of western North Carolina’s residents.

Many of the people affected by flooding from hurricane Helene had no idea that their homeowner’s insurance did not cover water damage. In the world of insurance coverage, property damage from wind, for example, is covered in most policies but not damage from flooding. My wife and I pay for a separate flood policy on our condo in South Carolina. It is backed by FEMA and covers flooding that destroys the items people depend on for their survival, such as refrigerators, utilities and other essentials. We carry a separate policy from State Farm that covers furniture and other personal property. The State Farm policy premium in 2024 was $894. The FEMA-backed policy was $1,111. (Note: In 2024, our personal policy premium decreased by a few dollars; the flood policy increased by more than 10%.) Those two policies do not even cover any structural damage or destruction of our two-story condo, which is one in a building of six units. Through our condo association we paid yet another $5,540 last year to cover the potential total loss of the condo. This year we will pay $6,130, an increase of 10%.

Our condo is almost a mile from the Atlantic Ocean as the gull flies and, despite some past hurricanes that damaged our golf course, the condo has suffered no flooding in 24 years. But Pawleys Island, SC, is not Asheville, NC; we expect hurricanes and are under no illusion that some might be especially damaging. The folks near Asheville had to be cruelly shocked by the ravages of a hurricane from so far away.

Insurance companies do not factor that you paid all your premiums on time for decades or that you never filed a claim. Given the increasing numbers of natural disaster claims that they must cover, they can make the case to state review boards that they need to raise their rates. If they deem the risk to your home has increased sharply, they can even drop your coverage; there is not much you can do about it. Insurers have fled states like California and Florida, which have responded with some assistance for the suddenly uninsured. Florida, like California, set up what is essentially a state-run insurance provider to cover at-risk residents whose insurance companies had left the state. The premiums are typically higher than what the homeowners were used to paying, but at least they have coverage. Yet the payouts for any future catastrophic hurricanes might exhaust funds in the state pool, lead to higher rates for those in the state plan and, potentially, lead to higher taxes for all of the state’s residents. (Note: Florida levies no state income tax but the money to fund such shortfalls will have to come from somewhere.)

As I write this, wildfires are raging outside of Los Angeles, leveling trailer homes and mansions alike. Many of the expensive homes are covered by California’s FAIR Plan whose ramifications, according to the San Francisco Chronicle, “could well be felt across California. Most obviously, the massive losses that insurers face could translate to increased rates for people across the state — particularly in the areas affected by the fires but also beyond…The [FAIR] plan has an estimated $24.5 billion in exposure across 15,300 residential and commercial policies in the ZIP codes impacted by the Southern California wildfires,” according to a Chronicle analysis of FAIR Plan data. Last summer, the FAIR plan held reserves of $385 million to pay for claims, according to the Chronicle.

A year ago, the bureau in North Carolina that represents insurance companies argued for rate increases that ranged from 4% in parts of the mountains to 99% in some beach areas. Increases in big cities like Raleigh, Charlotte and Greensboro that are popular with retirees and young families alike were expected at approximately 40%. Yet that was before most of the western part of the state was devastated by Hurricane Helene. In Buncombe County, which comprises Asheville, the rate-increase requests before Helene were for 20.5%. Residents of western North Carolina will almost assuredly have to prepare for more dramatic increases in the coming years.

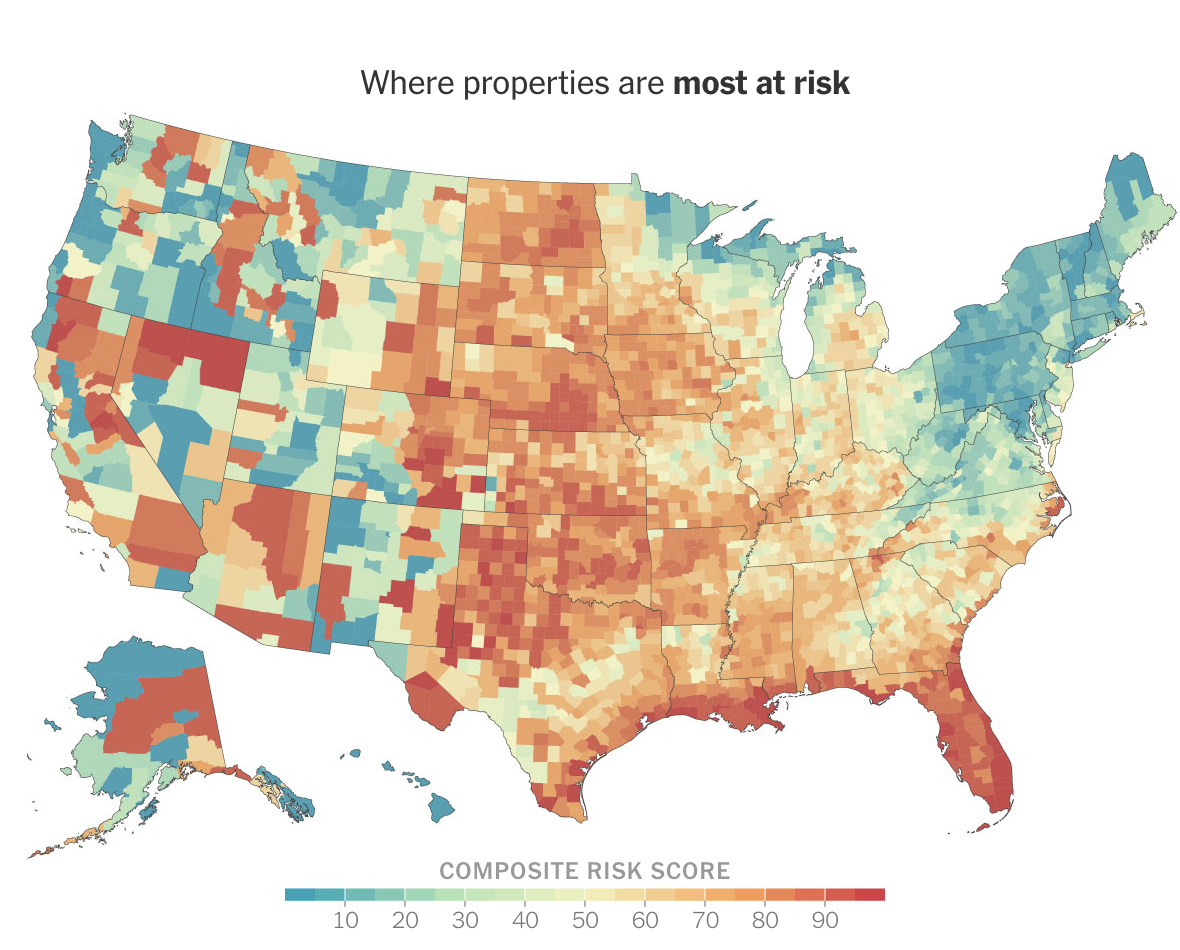

With natural disasters hogging the headlines across the U.S., are there any safe havens left? The map below pinpoints both the hotspots and the relatively safe spots across the land. Note that, in general, the highest risk locations are where retirees relocate for sunshine year round; and the lowest risk areas, like New England, are from where retirees have emigrated to avoid cold winters.

I also asked the following of ChatGPT, the artificial intelligence program: “Create a short article that identifies the places in the U.S. that are safest from the ravages of disasters, including hurricanes, flooding, tornadoes, earthquakes, wildfires and other natural disasters. List at least 10 places that are considered safe and where property insurance rates reflect those conditions.” Note that the 10 “safest” cities are almost exclusively northern; only Charlotte, NC, is in what is typically labeled “The Sunbelt.”

Here are the 10 towns that the program deemed safest, with some short rationales for the choices:

In early August 2023, my wife, my kids, grandkids and I spent a wonderful week on Lake Lure in North Carolina. That picturesque lake, where much of the movie Dirty Dancing was filmed, lies downriver from the town of Chimney Rock, which was decimated by flooding from Hurricane Helene last October. One local official put it this way to NBC News:

“…15 businesses were destroyed and 26 more were damaged. On the south side of town, 15 homes were obliterated and 14 more were damaged. Five bridges, including a footbridge, were razed. Three miles of Main Street, which is also known as U.S. Highway 64/74, were completely torn apart.”

The remnants of buildings torn apart by the flooding were carried down the Rocky Broad River to the circa 1927 dam that protects Lake Lure (photos below). The old dam held, but water carrying the flotsam and jetsam of the destroyed town overflowed the top and sides of the dam and turned beautiful Lake Lure into an unimaginable trash receptacle. Chimney Rock is located in Rutherford County, NC. A FEMA map detailing hazard risks across the country describe the Rutherford County risk as “relatively low.” (You can check out your own county here.)

Lake Lure, summer 2023

Lake Lure, October 2024

Most of the homes around Lake Lure sit at elevations well above the river and the lake. However, some were affected by reported mudslides. While watching my grandson on a putting green next to the community center at Lake Lure, I struck up a conversation with a retired couple who extolled the virtues of living in the community, including the climate. On reflection, it is a sad reminder of the Bob Dylan line: “Don’t go mistaking paradise for that home across the road.”

Think about it. If you love golf, when are you more relaxed and have more fun than on a buddy golf trip? A golf vacation is a time to dream, not only of a perfectly struck approach shot or a long putt for birdie, but also of how you might make the magic last for pretty much a lifetime. Making that dream a reality might be easier than you think – with a little help from your friends…er, buddies.

Since Myrtle Beach, S.C. is among the meccas for buddy golf in America – 80-plus golf courses, fair prices for golf and lodging, and easy to get to from major metropolitan areas – I am going to use it as an example of how a foursome might pool its resources, buy a modestly priced home and then use it, pretty much forever, as a group as well as with their families. In effect, four buddies with a dream can set up their own private timeshare in a golf community with all sorts of additional golf options within a short drive.

First the setup. For your next buddy golf trip, choose courses that are tucked inside residential communities – most courses in the Myrtle Beach area fit that description. Use one of the real estate sites like Realtor.com or Zillow and search the current listings for sale in those communities. Set a total price, to be split four ways, that will be modest for you and your buddies. In round numbers, I suggest condominiums and the occasional single-family homes that are priced at $400,000 and lower, making each friend’s investment $100,000 or less. Of course, there will be carrying costs that include taxes, homeowner association fees (if applicable) and, naturally, fees for golf. Virtually all golf courses along Myrtle Beach’s Grand Strand are accessible to the public but check if there are membership plans as well; you will be surprised at how modestly priced they are. Better yet, membership in one course often confers reciprocal play at many other golf courses in the area. (See reference to Founders Group International below.) A membership may be the smart way to go if, for example, you and your buddies intend more than one visit together annually, and if your families and you will visit at other times of the year.

You may get some pushback on the home front at first. Imagine that you return from your buddy golf trip and pose to your family the idea of investing in a home with your friends. “Who are you,” your spouse might respond, “and what have you done with my husband/wife?” (Note: More and more women are going on buddy golf trips, so this scenario could certainly be reversed to feature women golfers.) You might respond that the beaches on the Grand Strand are beautiful, accessible to all and within minutes of most any golf community you choose. Myrtle Beach is a resort town and exists to entertain families, not only with its beaches but also with plenty of activities for kids (aquarium, minor league baseball, a zoo at the famous Brookgreen Gardens). And dozens of the area golf courses offer a “Kids Play Free” program during the summer months. (I saved a lot of money in green fees for my nine-year old golf-obsessed son in the 1990s.) In short, the idea of a home in a golf community will mean much more to the family than simply golf for golf-obsessed daddy or mommy.

I looked at the latest listings for homes in some popular and reasonably priced Myrtle Beach golf communities. All listings are at least 3 bedrooms and 2 baths and are priced under $400,000. If you would like some specific help with identifying a golf home for you and your buddies, or just you and your family, please

Mike Strantz was one of the most creative golf architects in the history of the game but, at his death at age 50, he left only a limited number of designs that bear his particular – some might say “peculiar” – stamp. Although Tobacco Road in the Sandhills of North Carolina stands out as his most unusual layout, True Blue is unique as well. From above, the bright green misshapen fairways appear to have been laid down over acres of sand, so much sand, in fact, that cart paths run through most of the waste bunkers. It sounds more intimidating than it is, and given the wide fairways and huge greens, hit the ball straight and you can score well. (You can strike most shots easily from the tamped down sand.)

True Blue. Golf Club, Pawleys Island, SC

True Blue. Golf Club, Pawleys Island, SC

The condos adjacent to the golf course won’t win any creative design awards, but they are comfortable and among the most reasonably priced along the Grand Strand. This listing features three bedrooms and three baths over 1,400 square feet and terrific views of the golf course from the screened in deck. Priced at $359,000.

Myrtlewood and its 36 holes of golf – the Palmetto and Pinehills courses – is one of the oldest clubs in the Myrtle Beach area and is centrally located within just of few miles of dozens of other golf courses. The Palmetto, designed by the respected Ed Ault, was the first on the Grand Strand to be built beside the Intracoastal Waterway, and the entire length of the finishing hole runs along the water. Pinehills is the product of another renowned designer, Arthur Hills, who produces layouts that golfers love for their playability without being routine or boring.

I played the Pinehills course last summer, my first round at Myrtlewood since 1969 before any homes were built beside the courses. I was pleasantly surprised to see that the condo buildings have been designed with as much care as the golf courses were, not the usual “stack-a-shacks” that are eyesores on many layouts.

A three bedroom, two bath unit with lake views from its lanai and close access to Myrtlewood amenities is listed at the super-reasonable price of $298,000. Myrtlewood is one of the Founders Group International courses; therefore, Myrtlewood members have reciprocal access to the 22 other FGI courses, which include Pawleys Plantation, Grande Dunes, Kings North and TPC Myrtle Beach.

Some golf courses are more notable than their designers. Such is the case with Tidewater, one of the most entertaining layouts in the Myrtle Beach area. It was designed by Ken Tomlinson, a Columbia, SC, attorney and “amateur” golf architect whose only solo effort gained national recognition in 1990 as the best new public golf course in America from Golf Digest and Golf Magazine. Described by at least one reviewer as the [Kiawah Island] “Ocean Course without the blind shots,” Tidewater is as unique a layout as its designer.

Tidewater Golf Club, North Myrtle Beach, SC

Tidewater Golf Club, North Myrtle Beach, SC

There are relatively few condos in the Tidewater community that have been listed in recent years at under $400,000, but this one – at $399,900 – offers views of a pond and the Intracoastal Waterway. The three-bedroom, three-bath condo is an end unit, giving you total privacy on one side, and is offered almost fully furnished (except for a grandfather clock and some kitchen appliances).

With its four golf courses designed by some of the most notable architects working today, a foursome of buddy golfers would hardly have to stray off campus to find any other challenging and entertaining rounds of golf. The layouts by Norman, Fazio, Love III and Dye provide one of the widest range of experiences in one place on the Grand Strand. And the resort’s central location means shopping, entertainment, restaurants and the Atlantic Ocean beaches are within minutes.

Barefoot Resort, Love III Course, Myrtle Beach, SC

Barefoot Resort, Love III Course, Myrtle Beach, SC

This three bedroom, two bath condo is located in the Harbor Cove section of the resort and features views of the inland waterway from the master suite, a large balcony overlooking the Greg Norman golf course, and a transferable golf club membership. It is listed at $389,900.

The Crow Creek Golf Club is celebrating its 25th year in operation. It was designed by Rick Robbins, who cut his teeth working for the Nicklaus organization in China before going out on his own in 1991. He is credited with designs all over the world, including in his native North Carolina. He designed the golf course at Compass Pointe in Leland, near Wilmington, NC. (I played Compass Pointe shortly after it opened in 2016, and Robbins drove out in his golf cart to have a chat with me about his easygoing layout. Nice guy, solid golf course designer.)

This first floor, three bedroom, two bath unit is close to the golf course as well as the clubhouse and pool. It is priced at a reasonable $283,500.

Thanks for reading,

Larry Gavrich

Founder & Editor

Home On The Course, LLC